- Analyzed Investing

- Posts

- The S&P 500's Shaky Relief Rally, China’s Nuclear Leap, and the Hormuz "Bitcoin Toll" 🛑

The S&P 500's Shaky Relief Rally, China’s Nuclear Leap, and the Hormuz "Bitcoin Toll" 🛑

While Wall Street celebrates a 7-day winning streak, the plumbing is breaking. Explore the $20B private credit "gating" crisis, China’s 15-year lead in SMR nuclear tech, and how a new Bitcoin toll in the Strait of Hormuz is quietly dismantling the petrodollar. Don't get caught in the liquidity trap.

Analyzed Investing

April 10, 2026

In partnership with

The Private Credit Crisis

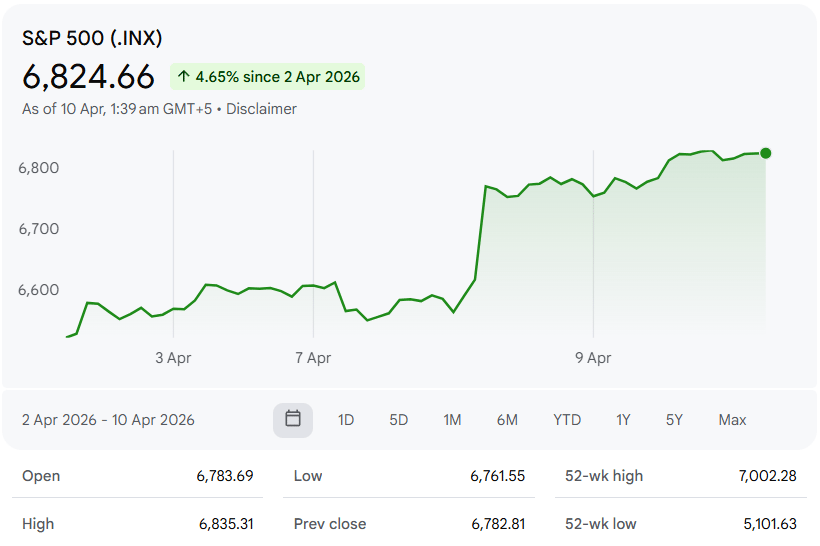

While the S&P 500's ceasefire-triggered relief rally seems like a victory lap, the structural floor of the market actually seems as flimsy as ever.

U.S. stocks have risen significantly since the start of the week, led by a 3.76% gain for the S&P 500. Both the S&P 500 and the Nasdaq Composite are currently on a 7-day consecutive winning streak.

While this may seem like the beginning of a victory lap, we actually feel that this is more likely the final exhale of a market in denial. The headlines are focused on the diplomatic "thaw" in the Middle East, but the plumbing of the financial system is currently screaming a very different message. While retail traders bid up the Nasdaq, the private credit sector is actually undergoing some severe stress.

Redemption Pressures: Some funds are imposing gates on withdrawals as retail investors retreat.

Valuation Concerns: Doubts surround how private credit firms mark their loans, with public Business Development Companies (BDCs) trading at discounts.

Performance Volatility: Publicly listed BDCs have seen share prices fall sharply.

Sector-Specific Vulnerabilities: Lending to small SaaS (software as a service) companies is under pressure.

Rising Costs: High interest rates are making it more expensive for borrowers to service debt, increasing the risk of default.

Regulatory Scrutiny: The Bank of England is conducting stress tests of major private lenders due to concerns about the lack of transparency in the $3.5 trillion market.

While analysts seem to be suggesting that this is not a full-blown crisis yet, some point out that the sector is navigating a much more challenging environment than in previous years.

In the first quarter of 2026, redemption requests for private credit funds hit a staggering $20.8 billion. Giants like Blackstone, BlackRock, and Blue Owl are being forced to gate their funds, honoring only a fraction of these requests to prevent a total liquidity collapse. When the "shadow banking" sector starts hitting its quarterly caps, it should be taken as a systemic red flag that the "soft landing" narrative has officially disintegrated.

The Blind Spot

The prevailing narrative on Wall Street seems to be that the Middle East ceasefire is the "all-clear" signal, inflation is a solved problem, and the Q1 earnings resilience proves the U.S. consumer is invincible. The consensus views this week’s 7-day winning streak as the birth of a new bull leg, fueled by the expectation that the Fed will eventually blink and return to a regime of easy money.

This narrative, however, seems dangerously detached from the underlying data. Here is why the herd may be walking toward a cliff:

1. The "Geopolitical Peace" Fallacy

The consensus believes the ceasefire in the Middle East has removed the primary tail risk for 2026. This ignores the delayed-onset inflation already baked into the supply chain. Urea and fertilizer prices haven't retreated with the headlines; they’ve decoupled. By the time the S&P 500 realizes that "peace" didn't lower the cost of food production, the secondary inflationary spike will already be crushing corporate margins.

2. The Liquidity Illusion

Mainstream analysts are pointing to "loose" financial conditions based on the Chicago Fed’s NFCI. What they are missing is the Private Credit "Gating" Crisis. While the public markets look liquid, the $1.7 trillion shadow banking sector is currently experiencing a silent run. When $10 billion in redemptions hit in a single quarter—and firms like Blackstone and Blue Owl have to restrict exits—it is a clear signal that the "structural floor" is actually a ceiling. You cannot have a healthy equity market when the debt markets beneath it are hitting emergency eject buttons.

3. The "Soft Landing" Mirage

The market is currently pricing in a "Goldilocks" scenario where rates stay high enough to kill inflation but low enough to keep the consumer alive. The data says otherwise. With 2-year Treasury yields at 4% (sitting stubbornly above the Effective Federal Funds Rate) the bond market is shouting that the Fed is "behind the curve" in the opposite direction.

Ultimately, the consumer isn't "resilient"; they are exhausted. With mortgage rates hovering over 6% and gasoline prices up significantly from January, the marginal dollar of discretionary spending has vanished. The consensus is buying the "relief," but they are failing to realize that relief is not growth. Investors are currently being lulled into a false sense of security by a concentrated index. While the S&P 500’s surface looks calm, the internal rotation into equal-weighted positions shows that the "AI-and-megacap" shield is finally cracking.

Stack BTC while you sleep

Tired of trying to time the market? YieldClub puts your money on autopilot. Deposit from your bank account, and your balance starts earning automatically, routing yield into Bitcoin around the clock. No charts, no timing the market, no crypto expertise required.

Signals, Noise, and What to Watch

🟢 Signal: Geopolitical Stagflation 2.0

The Conflict Premium: While a 45-day ceasefire proposal in the US-Iran crisis briefly sparked a relief rally early in the week, the reality remains grim. Tehran has already rejected the terms, insisting on full compensation before reopening the Strait of Hormuz.

CPI "Stag-Flationary" Print: The March Consumer Price Index (CPI) released on April 10 showed a sharp jump in headline inflation to 3.3% (up from 2.4%), driven by energy prices surging as high as $110 per barrel.

Economic Resilience vs. Costs: US nonfarm payrolls surprised with 178,000 jobs, but factory input prices have hit their highest levels since 2022, signaling that the inflation "bar" for a Federal Reserve pivot remains prohibitively high.

🔴 Noise: The "Ceasefire" Relief Rallies

Transient Optimism: Markets saw a 1.6% bump in the S&P 500 early this week on reports that diplomatic channels were opening.

Low Substance: This rally is largely driven by "geopolitical de-escalation narratives" and short liquidations (over $145M in Bitcoin shorts alone) rather than fundamental shifts. With the Hormuz deadline passing without a deal, this "bullish tilt" is increasingly disconnected from the physical reality of energy supply chains.

⚪ Watching: The Rise of Agentic AI in Core Settlements

Beyond Chatbots: While the world watches oil, major banks like Goldman Sachs and Lloyds are quietly moving from AI "assistance" to "transactional authority".

The Shift: These firms are deploying agentic AI—autonomous digital coworkers capable of settling trades and managing fraud investigations independently.

Market Impact: This shift toward "T+0" settlement and autonomous trading is expected to be a major differentiator in 2026, though it currently remains in the shadow of broader macro volatility.

China's Nuclear iPhone Moment

While U.S. investors are concerned about the trajectory of Fed rates, a shift in the global energy hierarchy may be taking place in China’s Hainan province. China is all set to commercially launching its nuclear future.

What is Happening?

China’s Linglong One (ACP100)—the world’s first commercial land-based Small Modular Reactor (SMR)—is currently in its final "hot functional trials" and is on track for full commercial operation by June 2026.

This is the first reactor of its kind to pass an IAEA safety review, and it has been built in a staggering 58 months. While the U.S. is still mired in regulatory paperwork and project cancellations (like the NuScale collapse), China has successfully industrialized the production of nuclear power.

Furthermore, the Shanghai Institute of Applied Physics recently confirmed a "world-first" scientific breakthrough: successfully converting thorium into uranium in a molten salt reactor. This effectively unlocks an energy source that requires no water for cooling and produces significantly less waste.

What it Means

"Western Lead" in High-Tech Energy Being Challenged: The U.S. is now officially 10–15 years behind China in SMR deployment. This is a capability gap that cannot be closed by subsidies alone.

Energy Export Hegemony: By having a "proven" and "operational" SMR, China is now aggressively pursuing export agreements with Indonesia, Thailand, Saudi Arabia, and Malaysia. These deals create 60-year dependencies for fuel, maintenance, and geopolitical alignment.

The AI Power Solution: SMRs are the "Holy Grail" for the AI boom. Their 125 MWe output perfectly matches the needs of a hyperscale data center. While U.S. data centers struggle with aging grids and "Not In My Backyard" (NIMBY) protests, China is building modular "plug-and-play" power hubs.

What to Watch

The July 4th Milestone: Watch for the U.S. Department of Energy’s "Reactor Pilot Program" results. They are racing to hit a criticality milestone by July 2026 to show the U.S. is still in the game.

Thorium Commercialization: If China moves from "experimental" to "commercial" thorium reactors, the global uranium market will face a long-term structural threat.

Belt & Road Nuclear Deals: Watch for official CNNC export announcements in Q3 2026. This will be the signal that China has successfully commoditized nuclear power.

A Bitcoin Toll on Hormuz?

The ceasefire a large section of the market is celebrating was supposed to clear the Strait of Hormuz. But while the S&P 500 rallies on headlines of peace, the actual plumbing of global oil trade has just undergone a permanent, crypto-fueled mutation.

While many believe that the flow of oil is returning to normal, the reality is very different. Iran is working to effectively institutionalized a $1 per barrel "Bitcoin Toll" for every VLCC transiting the chokepoint. By demanding roughly $2M per tanker in BTC—processed in seconds to bypass Western tracking—Iran hasn't just evaded sanctions; they’ve created a blueprint for the "de-dollarization" of energy.

This is the ultimate contrarian paradox.

While the White House pitches a "Bitcoin Superpower" future for the U.S., our adversaries are already using that same technology to dismantle the dollar's status as the global energy unit. With Iran’s crypto ecosystem hitting $7.8B, we are moving from a world of "free trade" to a world of "digital tolls."

If the U.S. responds by joining this "toll collection" system (a concept already being floated) it signals the official end of the era where the U.S. Navy guaranteed free, dollar-denominated global trade. This isn't just a temporary shipping delay; it is the birth of a sovereign crypto-tax on the world’s most vital commodity.

The Play: Watch for a structural floor in Bitcoin regardless of Fed policy, and prepare for a "permanent" $1–$2 premium on WTI crude that no ceasefire can remove.

The Contrarian Sentiment Gauge

Be honest: What’s your conviction level on the S&P 500's 7-day winning streak? |

The Bottom Line: Preparation Over Prediction

The market is currently intoxicated by the optics of "peace" and a seven-day winning streak, but as we’ve explored, the structural integrity of the financial plumbing is failing. Most investors are currently positioned for a "Goldilocks" scenario that the data no longer supports. When the "soft landing" narrative finally meets the reality of the private credit ceiling, the rotation out of speculative AI-caps and into essential stability won't just be a preference—it will be a survival mechanism.

In an environment where liquidity can be "gated" overnight, we are shifting our focus away from vulnerable SaaS multiples and toward the "plumbing" of the real economy. For those looking to navigate this volatility without constantly staring at a terminal, we are increasingly leaning on automated logic that prioritizes fundamental resilience.

Specifically, we’ve been refining a Recession Resistant approach within the Surmount ecosystem. By systematically rotating into defensive sectors—think consumer staples, healthcare, and utilities—the goal is to ensure that even if the "soft landing" turns into a hard one, the portfolio remains anchored by companies that provide the essentials the world can't quit. In a market built on flimsy floors, sometimes the most "alpha" move is simply refusing to fall through them.

Until next week,

Analyzed Investing

Want more like this?

I publish deeper dives and contrarian macro analysis at AnalyzedInvesting.com.

You can also find me on StockTwits and X.