- Analyzed Investing

- Posts

- The "American Exceptionalism" Trade Is Cracking — Here's What Fills the Void

The "American Exceptionalism" Trade Is Cracking — Here's What Fills the Void

Investors are actively reassessing their exposure to U.S. assets one year after Liberation Day, with global fund managers rotating away from American equities at a record pace.Most investors are still overweight U.S. large caps out of habit. The structural case for international value stocks, energy exporters, and dividend-heavy non-U.S. markets is stronger now than at any point since 2008.

Analyzed Investing

April 03, 2026

In partnership with

What "American Exceptionalism" Actually Was (And Why It's Ending Now)

This week marks one year since Liberation Day. The anniversary has generated the predictable wave of retrospectives, most of them focused on tariffs, the brief market panic, and the subsequent rebound. What almost none of them are asking is the more uncomfortable question: did Liberation Day expose something that was already broken?

The narrative of American exceptionalism — the idea that U.S. equities deserved a permanent premium over the rest of the world — was the single most consensus trade in global finance for fifteen years. U.S. equities grew from representing 45% of global market capitalization in 2009 to approximately 65% by 2025. Investors who questioned this were wrong for so long that most eventually stopped questioning it. That is precisely the moment to start.

Here is what the exceptionalism story actually was, stripped of mythology: it was the product of three specific, now-expiring tailwinds that had little to do with America being structurally superior and everything to do with America being in the right place at the right time.

The first tailwind was free money. The extraordinary monetary policy responses to the financial crisis and the COVID-19 pandemic injected trillions of dollars into the economy and kept interest rates near zero for over a decade. Low rates are a supercharger for long-duration growth assets. They make future earnings worth more in today's dollars.

The Magnificent Seven did not become the most valuable companies in human history because they suddenly got twelve times better at their businesses. They got re-rated upward by a mathematical function of the discount rate. When the Fed finally broke from zero, that tailwind became a headwind. Most portfolios have not yet adjusted to that reality.

The second tailwind was the AI narrative arriving at exactly the right moment. Just as rate hikes threatened to deflate the mega-cap multiple, the ChatGPT moment injected a new story: these companies were not just dominant today — they were going to own the future. The superior fundamental performance of the S&P 500 over the past fifteen years is entirely attributable to mega-cap technology stocks. The rest of the S&P 500 has not shown particularly impressive fundamental performance, yet is still accorded a premium multiple.

In other words, American exceptionalism was really Magnificent Seven exceptionalism, and the other 493 companies were along for the ride. That is a much more fragile foundation than the consensus believed.

The third tailwind was everyone else's weakness. U.S. dominance was bolstered by weaknesses elsewhere.

Europe's stagnating population growth,

China's overinvestment in housing constraining economic growth,

Brexit diminishing the U.K.'s global relevance.

Capital did not flood into American equities purely because America was exceptional. It flooded in because the alternatives looked worse. That calculus is now shifting in ways that one Liberation Day anniversary article will not capture.

The same policy actions that supercharged U.S. financial performance since the global financial crisis are now unwinding. The debt-to-GDP ratio sits near its highest level in over sixty years, with interest payments now exceeding national defense spending. The dollar has weakened sharply. And perhaps most importantly, the political infrastructure that made America the default home for global capital — rule of law, institutional predictability, Federal Reserve independence — is now a variable rather than a constant. As one allocator from CNBC put it this week, "U.S. exceptionalism is still intact, but it's no longer automatic."

That last phrase is the most important one for contrarian investors. "No longer automatic" means the premium that global capital paid for U.S. assets (simply because they were U.S. assets) is being repriced. The data confirms it: U.S. stocks are now capturing just $26 of every $100 flowing into global equity funds, down from a peak of $92 in 2022. TradingView That is not a rotation. That is a regime change.

The standard response at this point is to remind you that America still leads in innovation, still holds the world's reserve currency, still houses the most liquid capital markets on earth. All of that is true.

The contrarian point is not that America is finished — it is that you are no longer being paid to wait for excellence that the market has already fully priced in. When everyone owns the same thing for the same reason, the risk is that the premium no longer stands out.

Put This Thesis to Work — Automatically

If the argument made so far resonates, the natural next question is: how do you actually execute a strategy built around adaptive allocation in a fast-rotating market — without watching every tick?

That is exactly what the RSI-Weighted ETFs strategy on Surmount is designed to do.

While most investors are still anchored to static allocations built for a world of U.S. mega-cap dominance, RSI-Weighted ETFs takes a fundamentally different approach. It uses the Relative Strength Index to continuously measure momentum across ETFs — and allocates more capital to whoever is leading, less to whoever is fading. No opinions. No anchoring bias. Just the data.

In a market defined by exactly the kind of rotation described in this piece — where leadership is shifting from U.S. large caps to international markets, real assets, small caps, and value — a rules-based, momentum-sensitive strategy has a structural edge over a static portfolio. It is built to move with the rotation, not react to it after the fact.

This is the practical answer to the trap outlined in Section 4. You do not need to guess which geography wins next quarter. You need a system that automatically tilts toward what is working and away from what is not — across the entire ETF universe.

RSI-Weighted ETFs on Surmount lets you do exactly that, hands-free.

Market Volatility Exposes Weak Delegation

When markets get shaky, advisors don’t just manage portfolios. They manage fear, questions, follow-up and a flood of client communication.

That’s where weak delegation gets expensive.

If meeting prep, paperwork, CRM updates and account admin still run through you, response times slip and the client experience takes the hit.

BELAY created the free Financial Advisor’s Delegation Guide to help you identify what to hand off, what to keep and how to stay client-facing without losing control.

Inside, you’ll learn how to reduce bottlenecks, protect responsiveness and free up more time for the work only you should be doing.

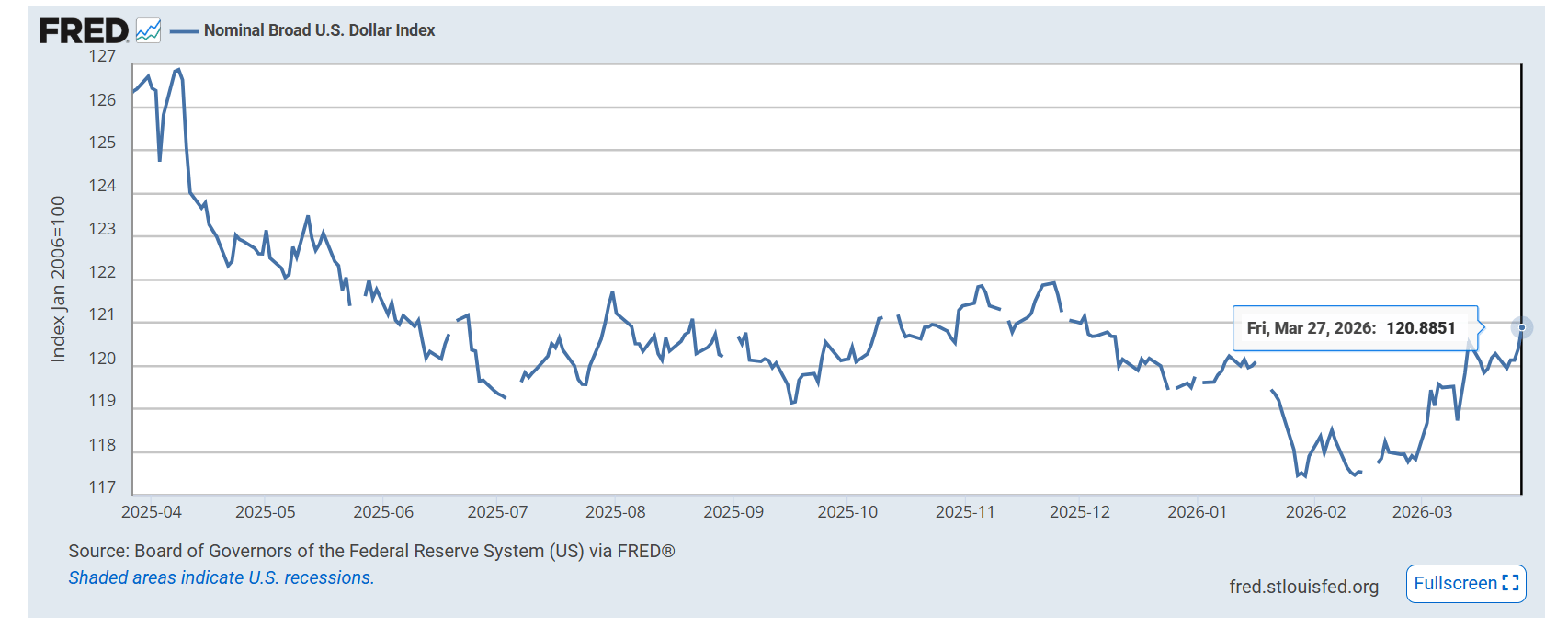

The Dollar Is the Sleeper Story Nobody Is Trading

Ask most investors what drove their returns over the past decade and they will name stocks, sectors, earnings beats, maybe the Fed. Almost none of them will mention the dollar. That is precisely the problem. The dollar is not a passive backdrop to your portfolio — it is an active return driver, and right now it is moving against most U.S.-centric portfolios in ways that the average investor has not begun to account for.

One year after Liberation Day, the conversation has been dominated by tariffs, sector rotation, and the death of the Magnificent Seven trade. All legitimate. But the dollar's slow-motion breakdown (a 13.5% depreciation against the euro, 13.9% against the Swiss franc, and 6.4% against the yen through mid-2025, driven by a mix of persistent structural pressures and new vulnerabilities) is the macro story that quietly compounds everything else.

This is what turns a decent international equity return into a great one. It is what is slowly eroding the real purchasing power of a U.S.-denominated portfolio. And it is what almost nobody is explicitly positioned for.

The Consensus Got the Tariff-Dollar Relationship Completely Backwards

When Liberation Day tariffs landed in April 2025, the near-universal assumption was that a more protectionist America would mean a stronger dollar. Tariffs reduce imports, reduce the supply of dollars flowing abroad, tighten the current account — textbook dollar bullish.

It was clearly wrong:

Historically, the U.S. dollar strengthens when U.S. Treasury yields rise. The reverse happened in April after the White House announced widespread tariffs — the dollar fell sharply even as yields spiked, as pointed out by Charles Schwab. Interestingly enough, tariffs did not make America a more attractive destination for capital. They made it a riskier one. Investors sold dollars because they were reassessing the outlook for the economy, and because President Trump's comments about potentially replacing Fed Chair Powell caused risk aversion to rise, with the U.S. appearing to be the source of the risk.

This is the key insight most investors still haven't absorbed. In a world where capital is mobile and the dollar's strength depends on global confidence in U.S. institutions and growth prospects, aggressive unilateralism is dollar-negative — not dollar-positive.

As a result, the tariffs didn't bring capital home. They sent it elsewhere.

.

Where the Capital Is Actually Going — And What's Still Cheap

Since U.S. stocks have fallen to their lowest share of global equity flows since 2020, the question worth asking now is whether the destinations still have room to run — or whether chasing them here is just a different version of the same mistake investors made piling into Nvidia at 40x.

The answer, as usual, depends on where you look.

Europe: The Fiscal Story Is Real, But Unevenly Priced

The headline that drove European equities higher last year was Germany's historic abandonment of its constitutional debt brake. The numbers behind that headline are genuinely significant.

Berlin has committed to €126.7 billion in investment for 2026 — the highest in German history — backed by €174.3 billion in borrowing and a €500 billion Infrastructure and Climate Neutrality Special Fund spread over twelve years. For a country that spent decades lecturing its southern neighbors about fiscal discipline, this is a structural shift (and not just a cyclical one).

The valuation case for European equities relative to U.S. ones remains intact even after a strong run. The STOXX Europe 600 ex-UK Index trades at 14.8 times 2026 consensus earnings — substantially cheaper than the S&P 500's 22.5 times valuation. The gap is wide enough that European stocks can absorb a fair amount of earnings disappointment and still look reasonable against U.S. alternatives.

Morgan Stanley's European equity strategists are forecasting earnings growth of just 3.6% for 2026, dramatically below the bottom-up consensus of 12.7% — a divergence that reflects a familiar European pattern of optimism that gets ground down by execution reality. The fiscal impulse is genuine, but infrastructure spending has tended to underdeliver relative to targets, and bureaucratic delays and skilled labor shortages could slow the pace of spending in 2026.

The smarter play within Europe is not broad index exposure but targeted positioning in the sectors directly in line with where the government spending is actually going — industrials, defense, and materials — rather than betting on a broad macro re-rating that may take years to materialize.

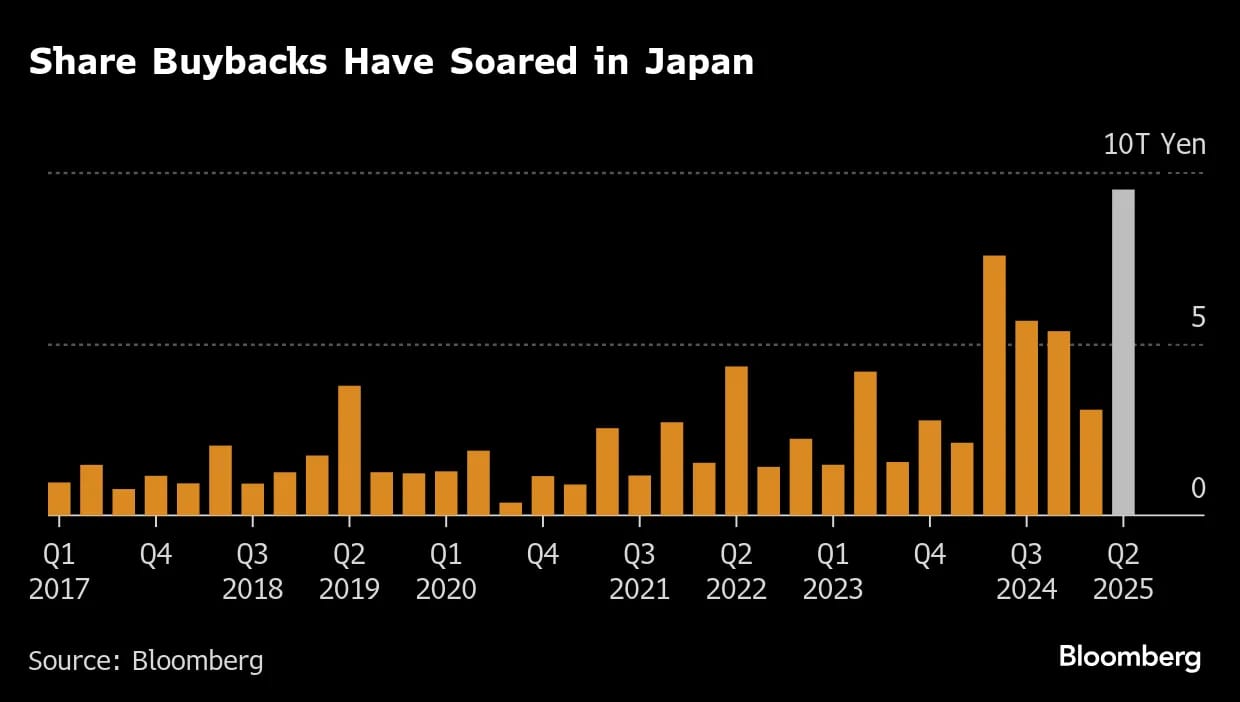

Japan: The Most Underappreciated Structural Story in Developed Markets

If Europe's investment case is about a fiscal awakening, Japan's is about something rarer and more durable: a corporate culture slowly being forced to care about its shareholders. A new revision to Japan's corporate governance code is targeting the $840 billion in cash held by listed companies, with draft rules that would require firms to verify they are using cash effectively. For context, that cash pile has been sitting largely idle for decades — the legacy of Japan's 1990s banking crisis, when hoarding became survival instinct and then simply became habit.

The Tokyo Stock Exchange's pressure campaign on capital efficiency is now moving from compliance exercise to tangible outcomes. Share buybacks, virtually non-existent in Japan 30 years ago, reached more than ¥10 trillion in the fiscal year ending March 2024, while dividends expanded from ¥2 trillion to ¥16 trillion over the same period.

This is not a story about Japan becoming Silicon Valley. It's a story about deeply undervalued industrial and financial companies slowly being compelled to return capital that was always there — capital that Western markets would have distributed years ago.

Morgan Stanley recently predicted that Japan could generate ROE of 13% by 2030 — a forecast that, if realized, could prompt a significant re-rating of Japanese equities. The opportunity is precisely that most Western investors still think of Japan the way it was in 2005 — a graveyard of value traps. The governance reform story gives those value traps an actual exit.

The Part Nobody Is Talking About: Where "Cheap" Actually Means Cheap

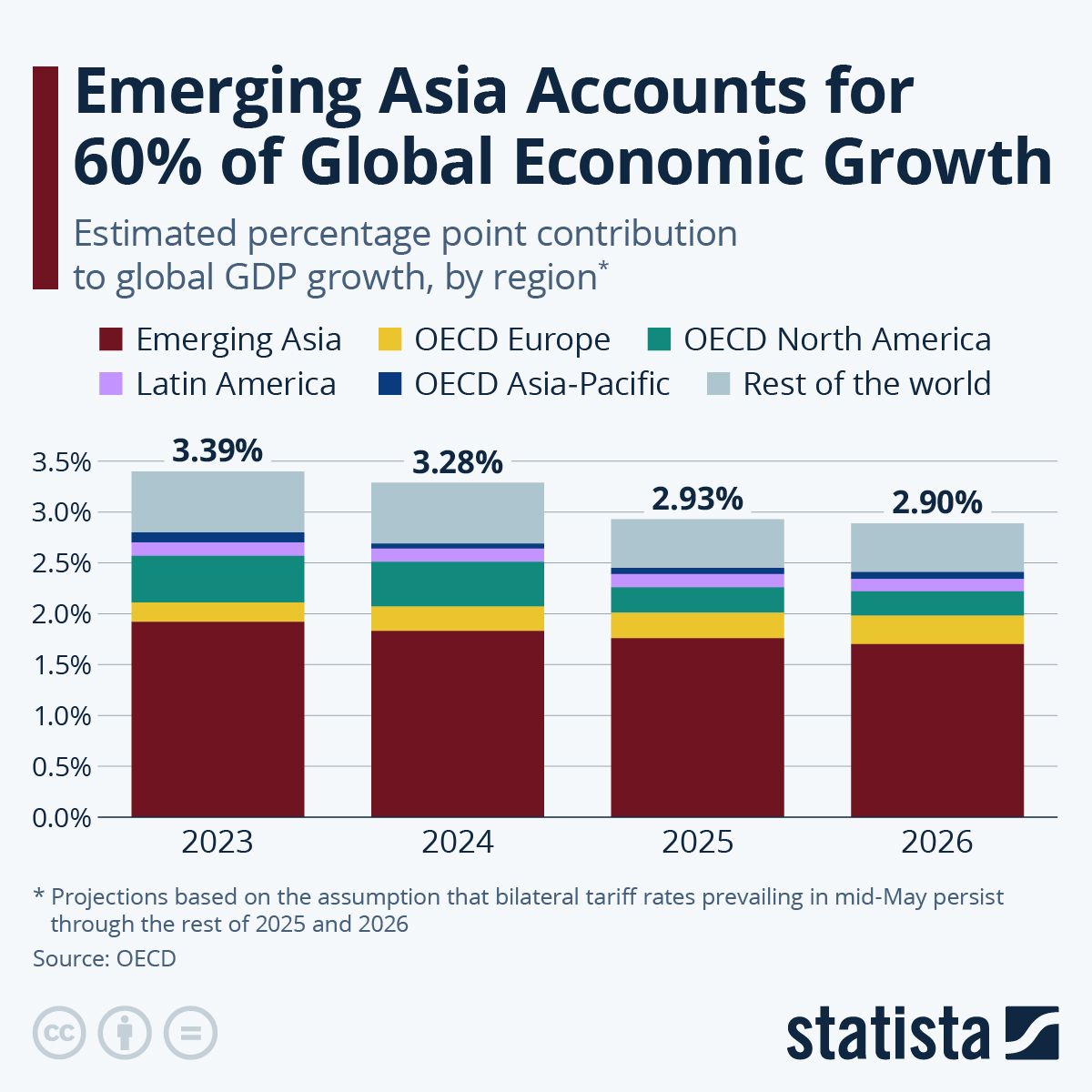

The loudest part of the rotation conversation is about Europe and Japan. But in 2025, the Morningstar Global Markets ex-U.S. Index rose 32% in U.S. dollar terms, with the European and Japanese rallies getting the bulk of the credit. The less-discussed destination for capital is the emerging market complex — and specifically the markets that are structurally positioned to benefit from the very forces that are hurting the U.S.: dollar weakness, trade route diversion, and commodity demand from infrastructure buildouts in both Europe and Asia.

Vietnam, Indonesia, and Mexico are emerging as high-growth hotspots in a world where companies are actively diversifying supply chains away from both the U.S. and China. These are not speculative bets. They are the logical downstream beneficiaries of a trade war that redirected manufacturing investment and a weaker dollar that inflates their earnings in U.S. terms. They are also the markets that institutional capital has been slowest to follow — which is typically where the best risk-reward sits.

Overall, Europe is real but partially priced. Japan is the most structurally interesting story in developed markets and still under-owned by most Western portfolios. And the emerging market beneficiaries of de-globalization remain the quietest part of a rotation that most investors are still only half-positioned for.

Why "Diversifying" Into What's Already Moved Is the Wrong Lesson

The irony of every major rotation is that by the time the consensus recognizes it, the easy money is gone. European equities are up sharply. Japan has been re-rated. Emerging market funds are seeing inflows for the first time in years. The financial press is running "Is This the End of American Exceptionalism?" as a cover story — which, historically, is precisely when you stop making that bet aggressively.

The wrong lesson from this moment is to mechanically reduce U.S. exposure and buy an international index fund. That is not contrarian thinking. That is just being late to a trade that institutional money already made in 2025.

The right lesson is more precise: what you are actually selling when you sell "American exceptionalism" is concentration in overvalued, dollar-sensitive, rate-dependent mega-cap growth stocks. That is a specific thing. And the hedge against it does not have to be geographic — it can be structural.

Small caps trading at a nearly 31% discount to their larger peers on a forward P/E basis represent a domestic alternative that benefits from the same forces driving international markets — lower rates, fiscal stimulus, dollar weakness — without requiring a currency bet or exposure to European political risk.

The contrarian position here is not "buy international, sell America." It is "sell the part of America that was never as exceptional as it was priced — and own the part that was always ignored." That is a harder trade to make. It is also the more durable one.

Until next week,

Analyzed Investing

Want more like this?

I publish deeper dives and contrarian macro analysis at AnalyzedInvesting.com.

You can also find me on StockTwits and X.